How to Improve Your Credit Score for Home Loan

Introduction:

Your credit score develops into your most essential life number which affects your home purchase plans for India. The score determines both your home loan approval status and your total interest payments for the next 15 to 25 years. Many buyers only learn about the score's value after they experience loan rejections or receive higher EMI offers. People should view their credit score as their financial standing among lenders. All lenders in India use this score as their primary assessment method for people who want to purchase a 2BHK apartment in Mumbai or a plotted development in Indore or a villa in Coimbatore. The market experiences rising property prices which results in 0.5 percentage point interest rate changes causing people to either gain or lose lakhs of money. The good news? People can enhance their credit score through simple methods which involve them to become more knowledgeable about their credit score and to maintain self-control and develop future strategies. We will present the information in this guide through an easy-to-understand and practical approach. The information here will assist both salaried professionals living in Tier 1 cities and self-employed buyers residing in Tier 3 towns to attain better financial conditions for their desired home.

What Is a Credit Score and Why It Matters for Home Loans

A credit score is a three-digit number, usually between 300 and 900, that reflects your creditworthiness. In India, scores above 750 are generally considered strong for home loan approvals. The situation becomes fascinating at this particular point. A good score provides you with two advantages because it aids your loan acquisition process while it improves your negotiation capabilities. The difference between interest rates leads to substantial savings because residents of Bangalore and Delhi require higher loan amounts. People in Tier 2 and Tier 3 cities can expect lenders to show some leniency in their approval process, yet their low credit scores will still restrict their borrowing choices. Banks view a high credit score as an indication that a customer will fulfil their financial obligations. The information indicates that you complete your payments on schedule while you handle your financial responsibilities and exhibit a high level of payment ability. A low score creates warning signals which result in increased interest costs or complete application denial. Before browsing listings on Property Aaj (https://www.propertyaaj.com), it’s wise to understand where you stand financially. Your credit score determines your purchasing power and the level of comfort you will experience when making purchases.

Common Reasons Why Credit Scores Drop

Many people think that their credit score dropped because they made one major error. The truth is that multiple minor behaviours create the actual problem. The most common reason for payment failure occurs through late payments. Your score will experience major damage from missing just one EMI or credit card payment. High credit utilization occurs when someone uses more than 30 to 40 percent of their available credit limit throughout the month. People in Tier 1 cities which have higher costs of living use credit cards excessively because they do not realize that this behaviour decreases their credit scores. People in Tier 2 and Tier 3 cities face payment difficulties because their self-employed income sources create payment schedule uncertainties. The common method of applying for multiple loans or credit cards within a short time frame represents an important factor that people neglect. The submission of each application results in a "hard inquiry," which causes a minor decrease in your credit score. Your credit report contains errors that occur with some frequency and these errors will result in an unfair drop in your credit score. Your report needs to undergo regular reviews because it serves as your protection.

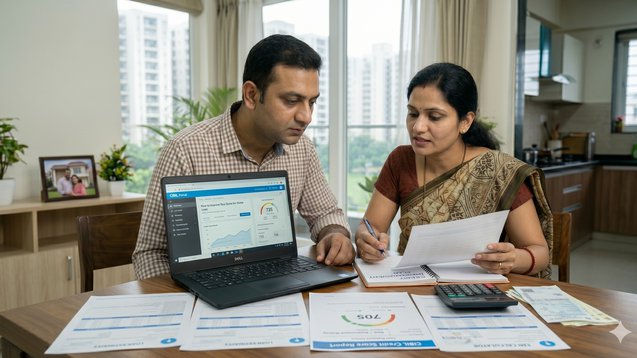

Start by checking your credit report.

You need to know what is going on with your credit report before you can fix any problems. The first thing to do is get a copy of your credit report from companies like CIBIL, Experian or Equifax. Look at more than your credit score. Check these things:

Any defaults or settlements

Payment history

Active loans

Credit card usage

Sometimes people find out that old loans are still showing up as unpaid even after they have been paid off. Fixing mistakes like this can really help your credit score. For example someone in Pune saw their credit score go up by 40 points by fixing a mistake on their credit report. This shows how important it is to make sure your credit report is accurate. Before you start looking at properties on Property Aaj (https://www.propertyaaj.com) make sure you check your credit report carefully. This will help you understand your situation and feel more confident when you talk to lenders. Checking your credit report gives you a picture of where you stand. Your credit report is like a report card for your credit history. So your credit report from companies, like CIBIL, Experian or Equifax is very important.

Pay Your EMIs and Bills on Time. Every Single Time

This might seem simple. It is the most important habit you can have, Your payment history is a part of your credit score. If you miss one payment it can stay on your record for a time. You should set up auto-debits for:

Credit cards

Personal loans

Existing EMIs

In cities like Tier 1 cities people are very busy and often miss their payment due dates. So setting up auto-debits is very helpful. In cities people are still learning about banking so it is very important to pay your bills on time. Think of it like this: when lenders look at you they are not just looking at what you did, in the past. They are trying to figure out what you will do in the future. If you make your payments on time it shows them that you are responsible and Pay Your EMIs and Bills on Time.

Pay Down Your Existing Debt Before Getting A Mortgage

If you are currently working on multiple loans there is a chance that these loans will hurt your chances for approval on a new mortgage loan. The amount you pay monthly (EMI) for existing loans will reduce the number of base points or degree that you qualify for as well. Banks have an internal scoring system called the FOIR (Fixed Obligation to Income Ratio). Banks will not lend if the FOIR is over (40% to 50%) of your monthly income (e.g. if your net monthly income is 80,000 and the total monthly payments you are making on existing loans and mortgages is 30,000, banks will significantly reduce your qualifications for a large mortgage loan). In particular Tier 1 Cities have higher home values than Tier 2 and Tier 3 cities so therefore the amount you need to borrow may be lower in Tier 2 and Tier 3 cities than in Tier 1 cities; however lenders will still favour applicants with fewer liabilities. There is a sound approach to reducing your existing debt. Make a priority of paying off all of your smallest personal loans so that you can improve your credit score and therefore increase the amount of money you can borrow

Maintain a Healthy Credit Utilization Ratio

Credit utilization simply means how much of your available credit you are using. Using credit at ₹1.5 lakh against your credit limit of ₹2 lakh shows a concerning pattern because you make timely payments. Experts recommend keeping utilization below 30%. In metro cities, where spending patterns are higher, this requirement becomes essential. But even in smaller towns, overuse of credit cards can signal financial stress. Request a credit limit increase only when necessary but do not use your extra credit to make additional purchases. The idea is to improve your ratio, not your expenses.

Try not to apply for multiple loans/credit cards all at once

Wherever you apply for a loan (or credit card), the lender will typically perform a credit check as part of their review of your application(s). Too many of these checks within a relatively short time may result in a reduction in your credit score. It also makes you appear to be ‘credit hungry’. Young buyers in tier 1 cities typically try different types of consumer finance products frequently and will be greatly affected by this practice. However, young buyers in tier 2 & 3 cities usually apply less frequently than the ones in tier 1 cities but are still encouraged to be conservative when applying for any new product. You want to plan your loan/credit card applications with care by only applying when absolutely necessary and spacing out the dates of your applications.

Keep Old Credit Accounts Open

The length of your credit history is important for your credit score. If you have a credit card or loan account and have always paid on time, keep it open. Closing it might make your credit history shorter. Think of it like a record of how you pay back money. The longer you have a record the more lenders trust you. For people buying a home who are looking at long-term investments, on Property Aaj this is especially important. A stable financial history helps when you are investing in property. A good credit history shows lenders you can manage your money well. It also helps you get loan offers when you want to buy a house or property. It is an idea to have a balanced mix of credit. If you only have one type of credit like credit cards it can hurt your credit score. A good credit mix includes things like:

loans, such as a home loan or a car loan

Unsecured loans, such as a personal loan or credit cards

This shows the people who lend money that you can handle different types of credit in a responsible way. In India a lot of people who are buying something for the time in smaller cities may not have much experience with credit. Building a manageable credit portfolio before you apply for a home loan can really help your credit profile. Having a credit mix, like a home loan and a credit card can make a big difference. A balanced credit mix is important because it shows that you can manage types of credit like secured loans and unsecured loans responsibly.

How Long Does It Take to Improve Your Credit Score?

This is the question everyone asks and the answer depends on your starting point. Minor improvements which include reducing credit utilization and correcting errors will show results within a 30 to 60 day period. The time needed to recover from major issues which include defaults and settlements extends to a minimum of 6 months and can last for more than 12 months. The key is consistency. The credit scores require time to develop but they provide better results for people who maintain regular habits. You should begin improving your credit score immediately because your property purchase will occur within the upcoming year. The property research period required by your research project matches the time required for property research on Property Aaj (https://www.propertyaaj.com).

Perspective on Tiers related to how much of an impact Credit score has all over India

In Tier-1 Cities, house prices are high, requiring larger loans. A small credit score increase will allow lenders to offer lower rates, providing thousands of rupees in savings throughout the term of your loan.

Tier-2 Cities have rapid-growing Markets for Housing, resulting in many competing lenders. A great credit score in Tier 2 will provide you access to better prices and a faster response.

In Tier-Three cities, with an increasing number of Banks opening locations, credit scores will become increasingly important to buyers. Most first-time homebuyers do not realize this and are often delayed as a result of their lack of knowledge about credit scores. A constant throughout all Tiers is that a borrower's credit score heavily influences their financial comfort after purchasing a residence.

Conclusion

Your credit score improvement process progresses beyond home loan qualification because it establishes a pathway toward your financial future which remains free of stress. Your score improvement enables you to obtain better loan terms because it decreases your monthly payments while increasing your chance of receiving loan approval. More important than anything else, it enables you to approach your purchasing activities with greater assurance. Homeownership presents people with both emotional challenges and financial responsibilities. Your lowest credit score will create the most unwanted pressure that you want to avoid. Start with a small task. Make your payments according to the scheduled time. Pay off your outstanding debts. Maintain your established routine. You can begin your next phase by visiting Property Aaj at httpswww.propertyaaj.com which offers verified property listings and information to assist your property selection process. A strong credit score functions as your pathway to home ownership because it enables you to enter your ideal residence with complete assurance.

FAQs

1. What is the minimum credit score required for a home loan in India?

Most banks require home loan applicants to have credit scores that reach 750 or higher. The lenders will approve loan applications which show credit scores between 650 and 750 but they will charge higher interest rates. The higher your score becomes the better your chances improve for getting more advantageous loan terms.

2. Can I get a home loan with a low credit score?

Yes, but it may come with higher interest rates or stricter conditions. You will need someone who has better credit to act as your co-applicant. The best strategy to follow for your application process requires you to raise your score before submitting your application.

3. How often should I check my credit score?

You should check your credit score every 3 to 4 months according to ideal guidelines. You should monitor your credit report regularly because it enables you to identify errors and track your progress which becomes crucial when preparing to buy a house in the next year.

4. Does closing a credit card improve my credit score?

The answer is no because this situation does not always work as expected. The process of closing a card results in two negative effects because it reduces your total credit limit while your utilization ratio increases which leads to a score drop. You should maintain your existing accounts as active because they contain beneficial credit history.

5. How long do late payments affect my credit score?

Late payments can stay on your credit report for up to 7 years. The effects of these payments will decrease after you establish a pattern of making timely payments.

6. Is it better to take a joint home loan for a better credit profile?

The loan qualification process becomes easier for you when you add a co-applicant who maintains a strong credit rating. Couples and families typically use this method in both Tier 1 and Tier 2 cities.