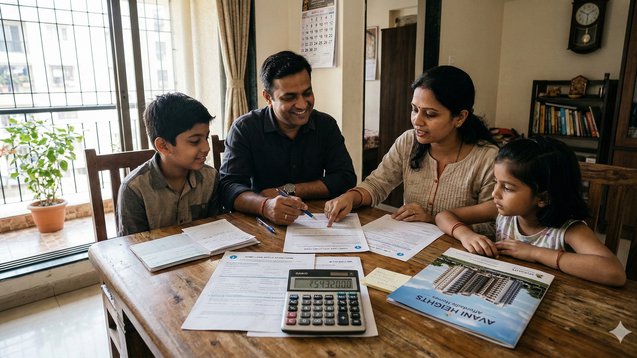

Introduction

The process of purchasing a house in India serves as an emotional milestone. The purchase brings homeowners both stability and pride which provides them with long-term security. The financial obligation underneath that emotional aspect requires a commitment period that lasts between 15 and 25 years which can extend even further. Many buyers make the mistake of assessing their financial situation through eligibility criteria while neglecting to check their ability to pay back their debts. The bank might grant you approval for a substantial home loan but that does not mean you should accept the entire amount. The rising property prices in Tier 1 cities such as Mumbai and Delhi NCR and Bengaluru drive buyers to select properties which include higher EMIs. Buyers in Tier 2 cities like Jaipur and Lucknow and Indore choose to exceed their spending limits because they expect their property values to increase in the future. The introduction of new townships and better transportation links in Tier 3 towns generates similar financial demands. The same problem exists throughout India because people tend to spend beyond their means when they try to acquire their ideal home. Before you make a final decision about listing your property on Property Aaj (https://www.propertyaaj.com), you need to assess whether the property meets your financial requirements and future objectives and personal preferences. A home should provide security to its residents but it should not create financial pressure.

Understand the Difference Between Loan Eligibility and True Affordability

Banks determine your home loan eligibility through four factors which include your income and your existing debts and your credit score and your ability to repay the loan. The higher pay scales in Tier 1 cities enable salaried professionals to receive larger loan amounts. People who need to qualify for a loan should understand that their eligibility does not ensure their comfort with debt. Financial advisors commonly recommend keeping EMIs within 30–40% of your monthly net income. Some buyers in Tier 2 and Tier 3 cities who face lower living costs choose to increase this ratio beyond its standard limit. Rising inflation together with medical expenses and lifestyle changes, creates a situation where cash flow becomes difficult to maintain. The Property Aaj website requires users to calculate both their EMI payments and their long-term financial sustainability before they can make property selection. You should evaluate whether your situation allows you to handle interest rate increases between 1 and 2 percent.

Factor in Hidden and Ongoing Costs

Your initial expenses increase because of stamp duty, registration charges, GST for under-construction properties, and brokerage fees, along with legal verification costs and interior work expenses. Different states apply different stamp duty rates. The states of Maharashtra, Karnataka, Uttar Pradesh, and Tamil Nadu establish their own stamp duty rates which include special concessions for women buyers in certain regions. Property values in Tier 1 cities create higher registration fees for their registration processes. The percentage fees remain constant in Tier 2 and Tier 3 markets but result in lower total expenses. The following expenses will occur repeatedly which include maintenance charges and property tax and electricity deposits and society sinking funds. Tier 1 cities with high-amenity projects require residents to pay high maintenance expenses. Premium societies in Tier 2 cities charge their residents extra fees for access to additional amenities. The complete budget needs to include all these elements in addition to EMI calculations.

Avoid Emotional Upgrades That Inflate Budget

The site visits allow visitors to become biased toward larger balconies and superior views and top-grade facilities. Your EMI payments will reach an uncomfortable level because the small increase requires multiple upgrades. The price per square foot for a 2BHK apartment increases when customers choose to upgrade to a larger space in Tier 1 markets. The "premium tower" option within the same project in Tier 2 cities results in extra expenses for residents. The residents of Tier 3 towns tend to pay excessive amounts for luxury features that have no effect on their property's resale value. The question "Can I afford this upgrade?" needs replacement with the question "Do I genuinely need this upgrade?"

Maintain an Emergency Fund Before Booking

Financial stability requires you to maintain cash reserves for property acquisition. You need to maintain six months worth of your basic expenses as separate savings from your home purchase deposit. Job markets in Tier 1 cities experience instability because of their IT and startup industry employment patterns. The job market in Tier 2 and Tier 3 cities offers less work possibilities to residents who experience income loss. An emergency fund protects you from loan default risk and emotional stress. You should maintain a portion of your savings for down payment expenses. The ability to adapt financially to various situations is more important than spending all your resources to acquire a larger residence.

Choose the Right Loan Structure

Indian home loan interest rates shift according to current RBI policies and prevailing bank lending practices. Although floating rates represent the common practice, these rates lead to increased EMI costs when they rise. Rate increases create greater financial burden for borrowers in Tier 1 cities who take out larger loans. In Tier 2 and Tier 3 cities, smaller ticket sizes reduce risk but still require careful planning. You should examine prepayment options together with foreclosure fees and loan duration. The extended duration of a loan results in lower monthly payments but higher interest expenses. The extended duration of a loan results in lower monthly payments but higher interest expenses. The right balance depends on your cash flow comfort. Property Aaj provides its customers with multiple lenders which they can use to evaluate different repayment plans before they make their final property purchase decision through its platform (https://www.propertyaaj.com).

Think Long-Term, Not Just Present Income

Your financial situation will undergo transformations throughout your life. Your spending patterns will undergo transformations because of your marriage and your children's educational expenses and your elderly parents' medical needs and your business activities and your professional development. People in Tier 1 cities experience lifestyle inflation because their incomes increase. Residents of Tier 2 cities see their monthly expenses rise when their aspirations to achieve more success about their social standing. People living in Tier 3 towns experience income instability when they shift from working locally to starting their own businesses. You need to project your expenses for property selection at least five to ten years into the future. Your ability to adapt to future situations will decrease if you exceed your current limits.

Rent vs Buy Considerations

Some Tier 1 micro-markets show low rental yields which create a disadvantage for investors who want to buy property there. Financially it makes sense to rent a better property while using extra money to invest in other areas. In Tier 2 cities the rental-to-price ratios create a fair system which makes homeownership more appealing to residents. People in Tier 3 towns typically buy property for personal use because they face difficulties finding rental options. The website Property Aaj (https://www.propertyaaj.com) allows users to compare local rental rates with their EMI calculations. When EMI payments exceed rent payments by a substantial amount, you should check whether the advantages of ownership offset the extra expense.

Avoid Comparing Yourself to Others

Home buying gets strongly influenced by peer pressure. Friends who choose premium projects create psychological pressure that compels others to follow their example. Social media usage helps people from Tier 1 cities to compare their lifestyles with others. The community visibility present in Tier 2 and Tier 3 cities usually leads to people copying others' actions. Your financial journey is unique. A 2BHK apartment that fits my budget provides better comfort than a luxury apartment which forces me to worry about my EMI payments.

Consider Appreciation Realistically

Many Indian cities experience property value growth from infrastructure development and metro connectivity and highway construction and IT park establishment. The process of property appreciation remains uncertain because it lacks any guarantees.Tier 1 cities show stable growth rates but their progress remains limited because they already maintain high price levels. Tier 2 cities may experience faster percentage growth in emerging corridors. The local projects create sharp but unpredictable value increases that affect Tier 3 towns. People should avoid using their entire financial resources to invest based on their belief in upcoming price increases. People should buy items that they can afford and which meet their needs instead of using them as investment tools.

Conclusion

The process of selecting a property requires you to maintain your financial limits because doing so protects your ideal home. A home should provide stability, comfort, and pride. The home must not generate financial worries during each month. You can defend yourself against urban cost increases through effective budgeting in Tier 1 cities. Tier 2 cities require this approach to maintain equal development while satisfying increasing needs of their residents. The system in Tier 3 towns protects residents from financial instability caused by unpredictable income. The process of searching for properties on Property Aaj (https://www.propertyaaj.com) requires you to assess both the property value and its environmental impact. You need to evaluate EMIs and hidden costs together with your upcoming objectives and emergency fund needs. Your ideal home exists. Beyond your most expensive home, which you can purchase, lies the property that, according to your financial situation, you can afford to own without risking your future financial stability and peace of mind.

FAQs

1. What percentage of income should go toward home loan EMI?

Financial experts typically recommend keeping EMI within 30–40% of your monthly net income. This approach enables you to handle all your financial obligations while saving money to achieve your long-term objectives without experiencing any financial difficulties.

2. Should I use all my savings for the down payment?

No. You should keep an emergency fund which needs to cover your essential living costs for six months. The practice of using all your savings to make a down payment creates financial risks which affect your economic stability.

3. How do stamp duty and registration charges affect budgeting?

These fees differ between states and they increase property expenses by 6 to 8 percent or higher. Buyers must include them in upfront budgeting to avoid shortfall during registration.

4. Is it better to take a longer home loan tenure?

A longer tenure reduces EMI but increases total interest paid. The suitable tenure should enable you to repay your debt through affordable EMI payments while keeping your total repayment expenses within limits.

5. Should appreciation potential justify stretching my budget?

Appreciation depends on market conditions and its future value remains unpredictable. The practice of purchasing assets beyond your financial limit based on anticipated price increases carries considerable danger.

6. How can I compare EMI with rent before buying?

You need to determine your monthly EMI and then compare it with the rental prices of similar properties located in the same neighborhood. Ownership advantages need to compensate for extra costs when EMI exceeds standard rent.

Read more about property matters with our specialists and browse the latest property listings on Property Aaj. Download the app from the Play Store and App Store now for easy buying, selling, and renting!