Introduction

People in India have regarded home buying since ancient times as a fundamental achievement which demonstrates personal success and provides lifelong security. People who choose to rent their homes experience three benefits which include flexible living arrangements and cheaper initial expenses and the ability to avoid lengthy rental agreements. People face a permanent decision between two opposing options which require them to choose between enjoying the benefits of renting or dealing with the responsibilities of home ownership. People believe that they understand the solution but it requires deeper evaluation. Your financial status together with your current job position and location and future objectives will determine your answer. Renting becomes the better choice for residents of Mumbai and Bangalore and Delhi because those cities have high property prices. People in Pune and Indore and Lucknow find home buying in their Tier 2 cities to be a possible option. People in Tier 3 towns find it easier to own property because of better access but they must still evaluate multiple factors. People need to evaluate all choices instead of following their first instinct about what to do. People who rent their homes today experience comfort but their current situation does not provide them with future benefits. People who own property start with stress but they gain their peace of mind for life. The information needs to be presented in an unbiased manner which avoids any exaggerated presentation so you can reach an informed decision which matches your personal requirements.

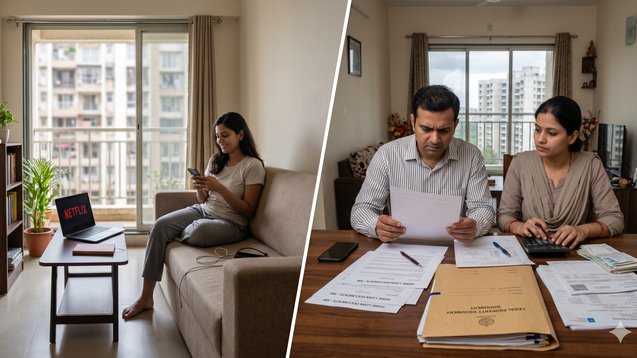

The Comfort of Renting Why It Feels Easy

The act of renting provides people with a freedom which they cannot attain through property ownership. You are free from ties which bind you to specific places and job positions and financial obligations which will last for several decades. The current work environment requires companies to adapt because their operational requirements are constantly transforming. In Bangalore and Gurgaon, young professionals can use renting as a way to find better job opportunities which allow them to commute shorter distances to their workplaces. You can improve your quality of life through upgrading your lifestyle after your job changes or you receive a higher salary because you do not have to handle property sales or extended loan repayments. People who rent their homes experience lower financial obligations during their first months of renting. The total cost of the property includes no down payment requirements and no stamp duty costs and no registration fees and no maintenance responsibilities which exceed fundamental costs. You spend your rent money while you handle your daily activities and then proceed to your next destination. The solution offers benefits that require less mental effort. The situation requires no monthly payments and there is no need to worry about property value changes and there are no concerns about the resale market. The ability to experience peace of mind brings significant value to numerous individuals. People need to understand that when they choose to experience comfort they will pay an unseen price. The present challenges of today find their solution through renting but the solution does not address the upcoming demands of the future.

The Hidden Cost of Renting Long-Term

The process of renting property appears to be simple, yet it fails to provide people with ownership rights. Every monthly payment goes to the landlord, not towards building your own asset.Over a period of 10 to 15 years, these costs will accumulate into a substantial total. Let’s take a simple example. Your monthly rent of ₹20,000 results in yearly expenses of ₹2.4 lakh. You have paid ₹24 lakh over 10 years, but you possess no ownership rights to show for your expenses. A similar EMI payment would have helped you achieve property ownership. The gap increases in Tier 1 cities. People who pay high rents experience greater financial losses throughout their lifetimes. In Tier 2 cities, where property prices are relatively lower, the difference between rent and EMI may not be very high, making buying more attractive. There exists a state of uncertainty in this situation. Rent increases pose a risk, landlords can demand tenants to leave, and tenants must relocate between different homes on multiple occasions. Families find the constant need to move between homes because of unstable housing arrangements to be extremely irritating. The doubts about their choice to rent begin at this point. The current situation provides comfort, yet the future holds uncertainty. Is it worth the investment?

The Pressure of Owning – Why It Feels Heavy

Homeownership creates entirely different difficulties which homeowners must handle. The primary obstacle which homeowners face is their financial obligations. A home loan is a long-term commitment which borrowers must repay for 20 years or longer. Buyers in Mumbai and Delhi cities spend a significant part of their monthly income on EMIs. This impacts how people choose to live their lives and save money and choose their jobs. People may feel “stuck” in their jobs because they need to maintain financial stability to pay EMIs. Homeownership requires multiple upfront expenses which include down payment and stamp duty and registration needs and interior design costs. These expenses reach 10 to 15 percent of the property value which represents a substantial amount. People experience psychological distress which extends beyond their financial circumstances. Homeownership limits your ability to move to different locations. Homeowners face difficulties when they need to sell their homes because sales do not happen quickly. The pressure people experience is genuine because it needs recognition as an urgent matter. The ownership of property results in negative outcomes for owners. The statement does not apply to all people.

Long-Term Wealth Creation – Where Ownership Wins

The ability to create assets through property ownership remains unavailable to renters who must face all financial obligations of their rental agreements. Real estate in India has shown consistent value growth because Indian cities continue to develop and expand their urban areas. The Tier 1 cities currently show high property prices, but the market demand remains strong. The property market in Pune and Ahmedabad Tier 2 cities experiences value growth because of their ongoing development of infrastructure projects. Investors who make their first investments in Tier 3 towns will discover that these locations provide them with multiple chances to earn high returns during the coming years. Your equity in the property increases with each payment because your EMIs represent more than just a financial obligation.Your loan balance decreases with time which results in your ownership of the property increasing. You will reach complete ownership of the property at its final payment date. The property has potential to generate both rental income and additional revenue streams through its rental activity. Your property will create secondary income for you if you decide to relocate to another city. Property Aaj (https://www.propertyaaj.com) provides buyers with tools to assess investment prospects through location comparisons and pricing analysis and future growth area examination which enables better ownership decision-making.

Lifestyle Flexibility vs Stability – What Matters More?

The decision process reaches its personal stage. Renting provides people with flexible living arrangements. Homeownership delivers people with constant security. Your current stage in life determines which option you should choose between these two choices. The best option for you is to rent because you need housing during your early career exploration period and your future plans remain unknown. The system enables users to make swift changes without incurring any financial expenses.People who possess a stable job and take care of their family together with their permanent city-based work obligations find home ownership to be an attractive option. People require stability and security together with a sense of belonging for their emotional development. Homeowners in Tier 2 and Tier 3 cities which experience less population movement tend to choose property ownership as their primary option. The job markets in Tier 1 cities maintain their current need for workers who possess flexible employment options. Different situations require distinct solutions. You must choose your housing option according to your life goals.

Comparing Costs – Rent vs EMI in Indian Cities

The rent versus EMI comparison shows different results in each city. The rental costs in Mumbai are usually lower than the EMIs which homeowners need to pay for the identical property, thus making renting a better option during the initial period. In Pune or Hyderabad, the gap is smaller, which enables people to purchase homes more easily. In some cases, EMIs may be slightly higher than rent, but the difference is not drastic. The majority of buyers choose to own property because they see better value in owning it for an extended period. Total cost calculation requires assessment of all expenses beyond monthly payment amounts. Home loans provide tax advantages, which homeowners should consider together with expected property value growth and rental rate increases.The Property Aaj website (https://www.propertyaaj.com) provides tools which enable users to assess multiple properties while determining their financial viability for purchasing a property in their selected area.

Emotional Satisfaction – The Value of Owning a Home

The emotional aspects of this decision cannot be fully measured through quantitative data. Home ownership brings people three important benefits which are pride and security and the ability to stay in their home. The emotional aspect of this situation exists as a powerful force in Indian culture. A home functions as more than a financial investment because it serves as a space where families develop their lives and create enduring memories and find their permanent foundation. The emotional bond to a location that brings comfort to people through renting does not exist in the same way for them. You have to follow specific rules because you are residing in another person's home which has particular boundaries. For many buyers, this emotional satisfaction becomes a deciding factor. It exists in a real way but its value cannot be quantified.

Risk Factors – What You Need to Be Careful About

Both renting and owning come with risks. The process of renting leads to two problems because it creates unstable conditions and results in continuous financial expenses that do not produce any ownership benefits. The process of owning a business brings three financial risks because it exposes owners to market changes and bad business decisions. In Tier 2 and Tier 3 cities, the two main risks involve two situations which either lead to slower property value growth or cause delays in building essential facilities. In Tier 1 cities, the risk is often overpaying due to high demand. The key is to manage these risks. Before you begin the process of home ownership, you should conduct thorough research to select the appropriate location and verify your financial capacity to handle ownership expenses. The website Property Aaj (https://www.propertyaaj.com) provides users with reliable tools to compare different projects and check the authenticity of listings, which helps them make better choices while decreasing their uncertainty.

When Renting Makes More Sense

There are situations where renting is clearly the better option. The process of buying property becomes burdensome when your job requires you to relocate frequently. Unstable income situations make long-term loans an unwise choice for borrowers. People should rent properties when real estate values exceed their financial capacity to buy. People should save money and invest their funds instead of trying to achieve financial goals through excessive spending. People choose to rent because they need short-term living arrangements while exploring their career options and maintaining financial flexibility.

When Owning Becomes the Smarter Choice

The better choice for you emerges after you achieve complete stability in your life. Financial security through stable employment, permanent residence in a city, and adequate funds for a down payment demonstrate strong financial capacity. The purchase option becomes more beneficial when your EMI payments approach your existing rent amounts. You are essentially paying for your own asset instead of someone else’s. The decision to own property becomes beneficial when you plan for retirement, establish family stability, and create long-term financial wealth.

Conclusion: It’s Not Renting vs Owning It’s Timing and Strategy

The choice between renting comfort and owning pressure does not involve determining right or wrong. The decision requires people to consider three things which are their present needs and their upcoming objectives and their planned methods. Renting provides users with two benefits which are short-term flexibility and short-term peace of mind. The path to financial success requires both rental and ownership options throughout your lifetime. The mistake many people make is choosing based on emotion or social pressure. You should focus on your existing personal circumstances. Where are you in life? What are your financial goals? How stable is your income? The decision process becomes easier when you respond to these questions with complete honesty. Property Aaj (https://www.propertyaaj.com) provides tools that enable users to evaluate different options and conduct property comparisons while making decisions based on factual information instead of guessed data. People look for ways to escape pressure and find comfort but that is not the main point. The process requires you to select the choice which benefits you reach today and in your future.

FAQs

1. Is renting better than buying in India?

The answer depends on your personal circumstances which require evaluation of your needs. Renting provides more flexible options which suit short-term needs, while purchasing property delivers permanent stability and long-term asset growth.

2. How do I decide between rent and EMI?

You should analyze your rent expenses together with your future EMI payments while assessing your income security and your upcoming financial commitments. Buying a property through EMI payments becomes advantageous when you can handle the EMI payments.

3. Does renting save money in the long run?

The answer is no because renting costs less during the initial period but it does not establish property rights for the renter. The property purchases will result in better economic advantages after a certain period of time.

4. Is buying property risky in Tier 2 or Tier 3 cities?

The answer depends on whether you select an appropriate location together with a trustworthy developer. The cities provide excellent growth opportunities when researchers conduct proper studies about their potential.

5. What is the biggest drawback of owning a home?

The primary disadvantage of homeownership involves the financial burden of EMIs which makes it difficult to change jobs or move to different locations.

6. Can I switch from renting to owning later?

Many tenants start renting before they buy property once their financial conditions improve due to better stability.

Read more about property matters with our specialists and browse the latest property listings on Property Aaj. Download the app from the Play Store and App Store now for easy buying, selling, and renting!