Introduction

Purchasing a house in Pune is a big step, and determining the right bank to approach for a home loan is one of the biggest financial milestones in this process. Because there are many nationalised banks and many private banks also offering competitive interest rates in 2025, it can be difficult to know which lender will suit you best. Besides looking at the rate percentage, buyers need to consider loan tenure flexibility, processing fees, top-up facilities, standard of service, eligibility to obtain the loan, and other features unique to the lender.

This comprehensive guide compares the best banks and housing finance companies with home loans in Pune on the basis of their latest rates, their typical customers, and key advantages. Also included are tips on how to choose a lender, FAQs, and opinions from experts.

Interest Rate Comparison – Leading Lenders in 2025

Public Sector Banks - Comprehensive Review

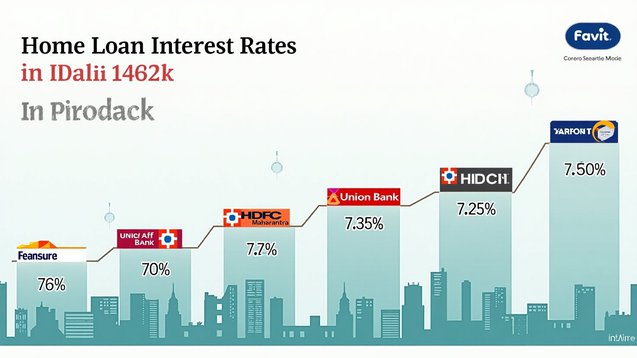

1. Union Bank of India (7.25%)

Low floating interest rates in 2025

Offers repayment tenure up to 30 years

Discounts for women borrowers and green home projects

Longer turnaround time but great stability in long term

2. Bank of Maharashtra (7.35%)

Focused on budget-conscious buyers and first-time home buyers

More relaxed eligibility if the property is located within Maharashtra

Requires up to ninety percent funding for eligible affordable projects

3. SBI (7.50-7.55%)

Most popular lender in India

Strongest networks, flexible documentation, and no hidden fees

Unique schemes for salaried professions, defence, and pensioners

Private Banks & Housing Finance Firms

4. ICICI Bank (7.70%)

Great processing times, possibility to have fully digital journey

Also attractive options for, balance transfer and top-up.

EMI begins only after full disbursement

5. HDFC Bank (7.90%)

Good support service, particularly for salaried buyers

Convenient option for apartment purchases in large gated communities

Less flexibility for self-employed income arrangements

6. Bajaj Housing Finance (7.35% - 9.20%)

Higher loan eligibility options based on assumed rent

Flexibility in EMI - part payments without penalty.

Excellent option for people buying in their first jobs.

7. IDFC First Bank (8.85%)

Specialized plans available for NRIs and startups founders.

Higher rate but flexible options for loan structuring.

Lower processing charges and faster disbursals.

Key Features to Compare While Selecting

Which Bank Should You Choose?

Looking for the lowest rate + long tenure?

→ Union Bank, Bank of Maharashtra, Bank of IndiaWant premium service + quick turnaround?

→ ICICI Bank, HDFC BankSelf-employed or flexible income structure?

→ Bajaj Housing Finance, IDFC First BankRely on public-sector trust and reach?

→ SBI or Canara Bank

Conclusion

In 2025, Pune homebuyers have an excellent choice of lenders, with interest rates ranging between 7.25% and 9.2%. Your decision should be based on three core factors – affordability (rate + tenure), eligibility, comfort, and service experience. Compare at least 2–3 banks, pre-calculate EMI burden, check long-term repayment ability, and negotiate concessions when finalising disbursal. Choosing wisely will save you lakhs over the course of your home loan.

FAQs

1. Which bank has the lowest home loan rate for Pune buyers?

Union Bank currently offers one of the lowest starting rates at 7.25% per annum, closely followed by Bank of Maharashtra and Bank of India at 7.35%.

2. Do private banks charge higher interest than government banks?

Generally, private banks start slightly higher (around 7.7%–8%) but compensate with faster approvals and better customer service. Public banks have lower rates but require more documentation.

3. How much home loan can I get based on my salary?

Lenders usually allow EMI up to 40–50% of your net take-home salary. So if you earn ₹1 lakh per month, you may get a loan where the EMI is around ₹40,000–₹50,000 a month, depending on tenure.

4. Can I transfer my loan later if another bank offers a lower rate?

Yes, you can do a balance transfer to another bank. Make sure savings from lower interest outweigh the processing and transfer costs.

5. Are interest rates expected to change in 2025?

Rates depend on Reserve Bank policy changes and inflation. If RBI hikes repo rate later in the year, floating rate loans may become slightly more expensive.

6. Is it better to choose a shorter tenure or a lower rate?

Lower rate reduces EMI instantly, while shorter tenure increases EMI but saves more money on total interest outgo. Choose based on your repayment comfort.

Read more about property matters with our specialists and browse the latest property listings on Property Aaj. Download the app from the Play Store and App Store now for easy buying, selling, and renting!